Deflation vs. Inflation

An exploration of why deflation is good, starting with a response to Peter Zeihan on Joe Rogan

Peter Zeihan: You can’t use a fixed supply currency because you get “monetary inflation” which makes the currency more expensive and “that is one of the fastest ways to destroy an economic model”.

This is wrong for several reasons. And said with such annoying confidence that my Sunday morning turned into writing this to explain why.

Backwards terminology

First and foremost, he has his terminology backwards – when he says “monetary inflation” what he actually means is “deflation”. He’s referring to the price of the currency unit increasing, aka “inflating”, so he uses that word. However, people who study currencies use these terms to denote the inverse measurement: how the price of goods track over time relative to that currency. An “inflationary” currency means that you have to spend more units of currency to buy the same thing over time (have you ever compared a menu of prices in dollars from the 1970s vs. today?). Conversely, a “deflationary” currency regime is when prices deflate over time and each unit of currency buys you more, not less. So, right off the bat, Peter Zeihan has his terms flat out backwards. Bitcoin is a deflationary currency.

Savings is the primary function of money

Next, Zeihan assumes that the primary role of a currency is to purchase goods with. We’ve broadly been conditioned to think this in the modern world, but that’s because our fiat currencies are simply unusable for the primary use case of a currency: serving as long-term savings. Zeihan states that a currency that is more and more expensive over time fails at what he assumes to be the primary function of a currency, transacting with. But, a currency that gets more and more valuable over time is outstanding as a currency for storing your savings in – better, in fact, than any currency in human history (which have all lacked the hardcapped supply feature and increasing scarcity function that Bitcoin is based on).

Not only is Bitcoin excellent at what is actually the primary function of a currency (being a good savings vehicle), but it also doesn’t matter for transactional purposes that Bitcoin gets more expensive over time. If a worker earns 3 Bitcoin per year today, and in a few years the value of Bitcoin has risen such that that same worker now earns 0.3 Bitcoin per year, it might feel like this currency isn’t working. But, if that worker experiences a 10x deflation in their wages, that’s because the cost of everything has also deflated 10x. Their standard of living hasn’t decreased, and that’s because it doesn’t matter how much a unit of currency costs… all prices in a system are relative. So there’s no such thing as a currency being “too expensive to use” as Zeihan suggests.

Inflationary currency regime vs. deflationary currency regime

Finally, there’s a deeper assumption that Zeihan is making that is simply wrong. When he concludes that a deflationary currency regime doesn’t work (incorrectly using the opposite term of “inflationary”), he is completely ignoring the realities of modern history. We have been in an inflationary currency system ever since the creation of Central Banking with the Federal Reserve in 1913. The first era (1913-1944) involved very minimal inflationary policy, the next era involved a good bit more (1944-1971), and the last has seen a great deal of inflationary monetary policy (1971-present).

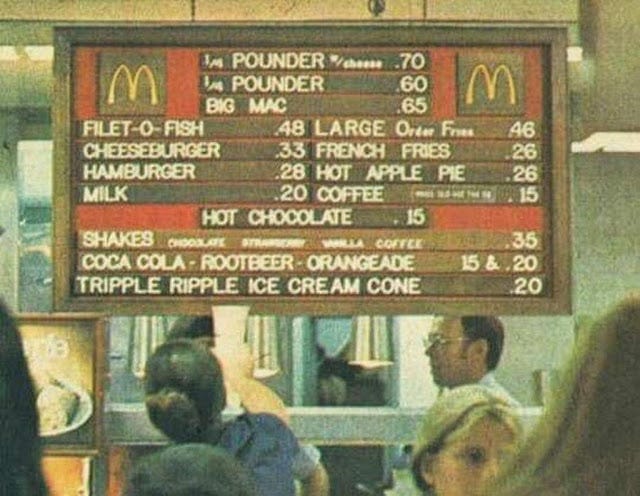

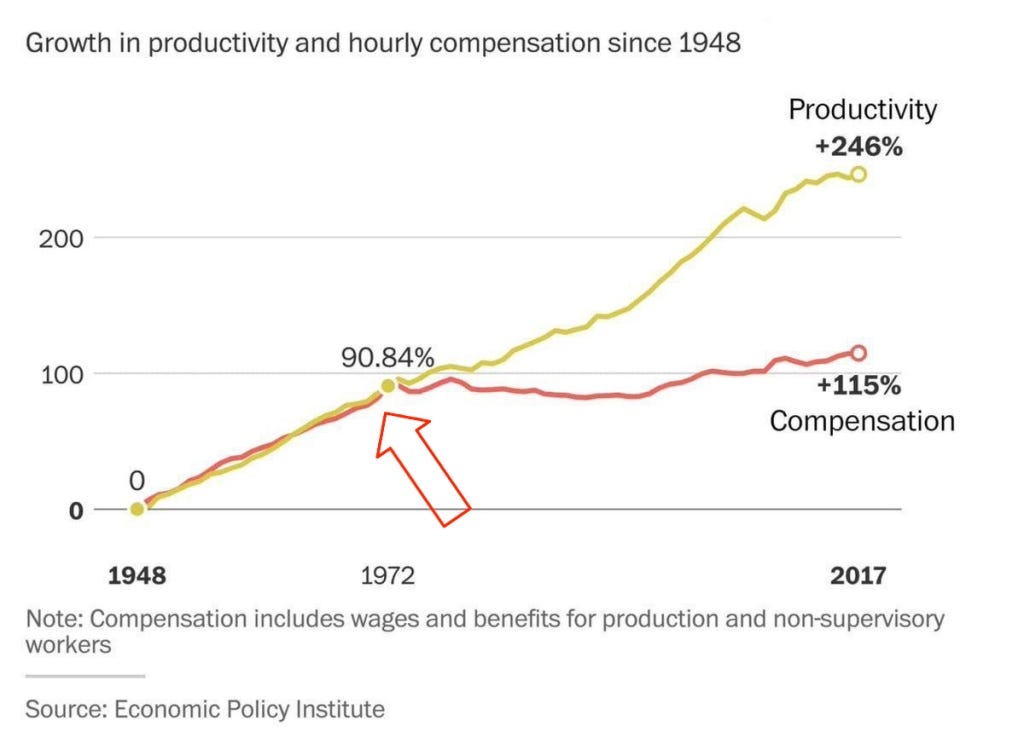

What have we seen as a society since 1971 in particular? (Explore some fascinating graphs here.) The erosion of middle class wealth and wages, and the explosion of asset prices which has disproportionately benefited the top 1%. This has also been the era of eroding quality in our goods – producers who seek to keep their prices flat are forced to either offer less product for the same price (shrinkflation) or cut the quality of their inputs (like replacing butter with cheap canola oil previously reserved for use as an engine lubricant). That’s what an inflationary regime looks like. You feel it all around you – it looks and smells like nihilism and despair and feels like the American Dream slipping further and further out of reach for each subsequent generation.

But do we have a good example of a deflationary currency regime in the modern world? Why, yes! Basically the 150-year time span between the American Revolution and the creation of Central Banking in 1913. Back then, gold was money, and there was no printing money because you couldn’t print gold and there was no governmental authority yet who could claim the authority to print unbacked promises against the gold that did exist. (That would come in 1913 when a lobby of powerful private bankers pushed the Federal Reserve Act through Congress via a short-notice vote during the Christmas holiday.) And what happened over that 150-year experiment? The global economy grew faster than the above-ground supply of gold. This meant that prices shrank over time – we got more for less – we had “deflation”.

And what did deflation cause? Well, in a deflationary environment, individuals are incentivized to allocate capital smartly to capital intensive projects that can drive an attractive return on investment. In that 150-year span, we had the Industrial Revolution. The steam engine enabled railroads. A few decades later, the internal combustion engine would give rise to automobiles and to airplanes. The world went from lanterns lit with whale blubber to electricity being piped everywhere and lightbulbs illuminating street and home.

Transatlantic correspondence went from a courier carrying a letter across the ocean to the telegraph and then the telephone. Modern science exploded with innovation – the germ theory of disease led to a revolution in healthcare while anesthesia ushered in modern surgery. And these same effects are seen in culture as well – where did culture find itself after 150 years of deflationary forces? Look no further than the craftsmanship of homes from the Victorian and Edwardian eras that linger today as living time-capsules. Generations of improving quality without having to raise prices compounded to drive excellence in every design aspect of the built environment. Craftsmanship reigned supreme, from grand interiors to functional details.

The great Impressionist painters (Van Gogh, Monet, Renoir) and sculptors (Rodin, Degas) that we hold up as a high-water-mark of artistry had their heyday at the peak of this Gilded Age that was quite directly the product of 150 years of gold-standard deflation.

These forces of craftsmanship and aesthetic excellence brought the advent of the Jazz Age and Art Deco movement before the countervailing forces of inflationary currency regime brought us the excesses of the 20s and the hangover of the Great Depression, the unlimited budgets of WW2 Total War (you can always print more fiat money), and the cheapification of everything post-1971. During 150 years of deflation, mankind benefitted from an ongoing feedback loop of prudent capital investments unlocking breakthroughs for the whole world.

Contrast this to what we’ve seen since 1971, which has been the relentless bidding-up of asset values. This happens because of the coincidence of two simple drivers. First, when you print lots of money, you are willing to accept lower rates-of-return because there is so much money to go around that you have to say “yes” to more and more projects just to put that money to work somewhere. This drives down interest rates over time, which drives up the value of assets because you are discounting future cashflows from those assets less when your interest rate is lower. Asset values go up! Second, in an environment where you are printing lots of money, the currency loses its effectiveness at the primary function of money: to store value for use in the future. As a result, inflationary currency regimes actually “demonetize” the currency, and it becomes prudent to store value in assets that are harder to inflate the supply of – real estate and equities, chief among them. Furthermore, you know that because more units of currency are being created every year, the nominal value of scarce assets will increase over time. This incentivizes people to take on leverage to juice those reliable nominal returns. As a result, while the winning formula for wealth creation in a deflationary environment is to invest in promising research & development projects, the winning formula in an inflationary environment is to take on a ton of debt and bid up real estate (sound familiar in the last ~40 years or so?). Make no mistake, this is why the median house in 1981 cost 2x the median income, whereas today the median house costs 10x the median income.

Learn more

If you found this interesting or confounding, subscribe to my free Substack for more:

I also highly recommend you read the excellent and thoroughly engaging “The Price of Tomorrow” by Jeff Booth to learn more about inflation vs. deflation, and “The Bitcoin Standard” by Saifedean Ammous to learn more about the lessons of monetary history.

Excellent piece! Great book recommendations; read them both and just finished Fiat Standard as well.

Great read.

Many of us have had visceral reaction to Peter's gibbirish, a properly articulated explanation to his cognitive dissonance is welcomed, big up !